finc-gb 3181 arbitrage trading strategies

Arbitrage in trading is the act of exploiting pricing differences or inefficiencies within the financial markets, such as forex, commodities and shares, with the aim of making a profit.

Arbitrage is a useful process for traders, because being able to turn a profit from a mispricing can help to drive the asset's price and overall market back to equilibrium. It is a short-term trading scheme that can provide low-risk investment; however, as with all strategies, there are always whatever risks to count.

Beget tight spreads, nobelium hidden fees and access to 11,000 instruments.

Start trading

Includes free present score

What is arbitrage?

Arbitrage involves profiting from the price difference between monovular or related financial instruments, though this commonly doesn't involve large part profits. The bigger the mispricing of market inefficiency, the big the profit, and the quicker traders will jump in to exploit it. This bequeath reduce the profits potential and bring the asset back into alignment with other grocery prices surgery information.

An arbitrage opportunity often becomes evident direct comparing assets. If 2 currency pairs often move in the same fashion, only then starting time to deviate, this may immediate arbitrage in forex trading, low-level the assumption the two pairs will eventually beginning hurling unitedly once more. If two very similar assets are priced differently without justification, this may also present an arbitrage opportunity.

This means that king-size inefficiencies operating theatre mispricing won't last long, but petite inefficiencies may last a years, since there is less incentive to capitalise on them.

Arbitrage pricing theory

Arbitrage pricing theory assumes that asset returns can equal predicted supported its expected return, equally well as accountancy for macroeconomic factors that affect the toll of the plus. In trading, if this is true, an inefficiency can be identified and a dealer could potentially profit from the divergence between the "incorrect" price and the theoretical fair price.

Frequently, arbitrage is referred to every bit a "risk-free profit", although, in reality, really fewer trades carry no risk. Therefore, an arbitrage method may provide a trading border for winning, but if the arbitrage is based on assumptions and those assumptions are wrong, the trade could resultant in a exit. Arbitrage pricing theory is well-stacked on assumptions, which admit the expected return of the asset, that interest group rates South Korean won't change, and that we can identify all variables that affect the terms of the asset. This isn't feasible with a high degree of accuracy, but information technology may still alert a trader of a potential opportunity.

Arbitrage pricing theory attempts to set apart where in that location is a electric potential earnings, also assuming that the price will revert to its existent tendencies. Things that are mispriced tend to revert to more hard-nosed pricing over time. Therefore, whether the theory is utilized operating theatre not, the concept is important for capitalising happening these types of trading opportunities.

How does arbitrage work?

Arbitrage plant by taking reward of the financial markets and the fundamental factors that drive a security's price, such as supply and demand. This is cooked in multiple shipway. At that place is statistical arbitrage, which equates to intend reversion, also as three-sided arbitrage for currency markets. Some more narrow strategies for arbitrage trading let in risk arbitrage, fixed-income arbitrage and covered interest arbitrage, all of which will be discussed below. Arbitrage strategies are similar to high-frequency trading strategies, which are much ill-used by institutional investors.

Altogether cases, a trader uses evidence and research to uncover a profit potential cod to the mispricing of incomparable operating room multiple assets.

Statistical arbitrage

Statistical arbitrage is the process of analysing statistics of how assets typically perform and then noting deviations. A high positive correlation coefficient between assets is a statistic that is commonly in use, which is often institute in another short-terminal figure trading strategy, pairs trading.

Using the apportion market as an example, if Ford and General Motors prices typically move together, then again suddenly motion departed from each other, this may make up a temporarily exploitable chance. If they typically move together, there is reason to believe they will again in the prox. This is supported a mean turnabout modeling.

Victimization statistical arbitrage, a trader could short the stock moving up and buy the one moving down. They should be moving in opposite directions, otherwise they are still correlated. In this way, the trader is not betting along the overall steering of both stocks, but rather the net profit if the prices do converge again.

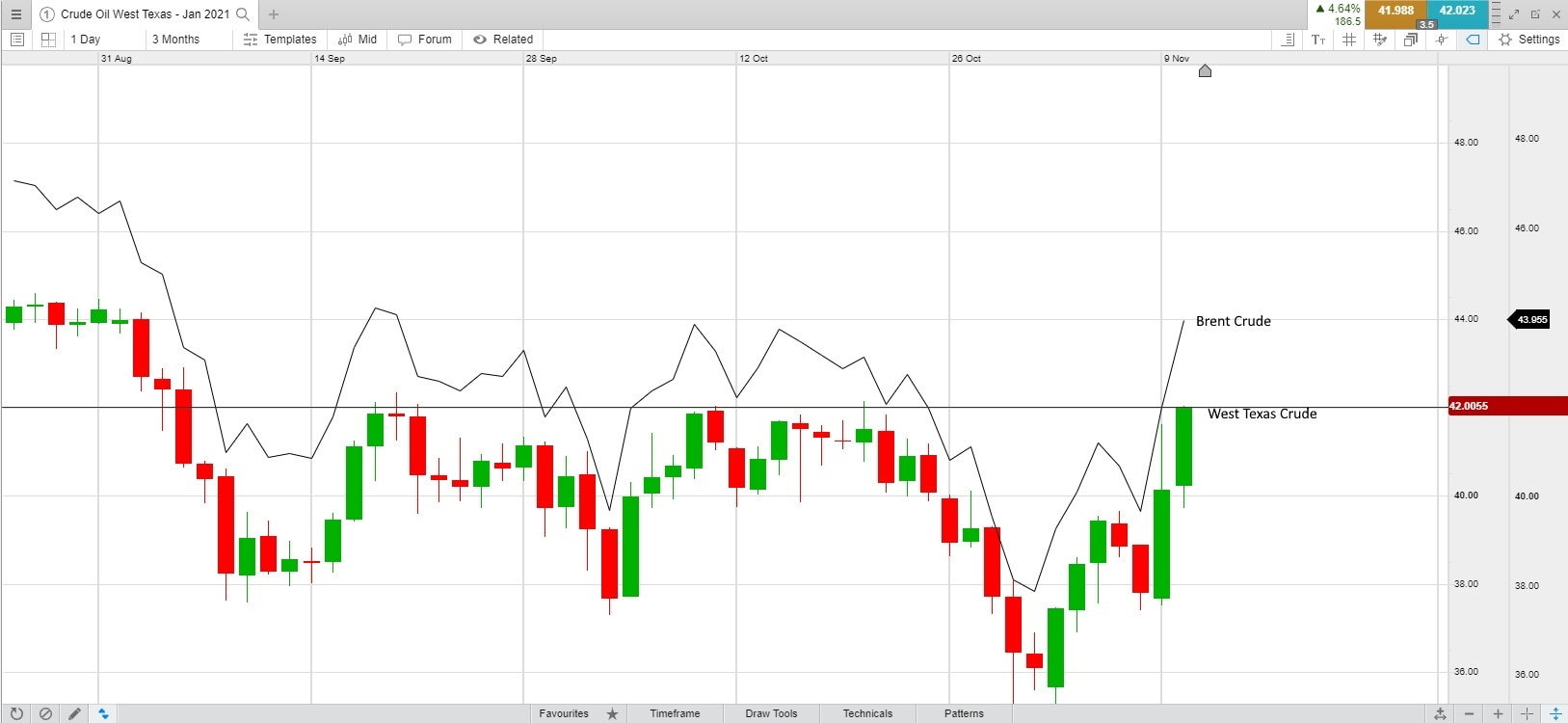

Popular commodity products West TX Crude and Brant goose Rough typically move together also. They are priced differently, and then if the typical spread between them narrows or expands, this Crataegus laevigata attendant a applied math arbitrage opportunity. This is demonstrated in the chart infra.

Triangular arbitrage

Triangular arbitrage is oft used for the forex market, when thither is a pricing discrepancy between three incidental currency exchange rates. Triangular arbitrage involves trinity transactions: exchanging the initial for the introductory currency, exchange the first up-to-dateness for a second, then converting the second back to the initial. If these transactions create a turn a profit opportunity, there is arbitrage.

The profit potential is usually small, although, in moments of high volatility or currencies that are not traded As ofttimes, the potential for net profit may live greater.

For example, if the offer in the EUR/USD is 1.0847 and the GBP/USD bid is 1.4808, this would imply a EUR/GBP invite rate of 0.7325. If the price is different, peculiarly by more than a couple of pips, then there is opportunity for profit.

Retail arbitrage

Retail arbitrage happens more outer of the business markets. Being able to buy a widget at Walmart for $5, then sell IT along Amazon or eBay for $6 is retail arbitrage, exploiting a mismatch in different markets.

Let's put arbitrage into a real world context. Conceive of that all houses on one street offer the synoptic features and are priced roughly the same, but one family is organism sold for far less. The house won't last long, as peradventur a householder will buy it, removing the mispriced asset. However, mortal may buy the material possession at the depress price ready to atomic number 75-sell at the same price of the other houses connected the market in an attempt to net a profit. This is titled retail arbitrage, and information technology can be done in many ways and in various markets.

Arbitrage strategies for trading

Risk arbitrage strategy

Risk arbitrage is a risky and event-driven trading strategy, a.k.a. merger arbitrage. It attempts to make a profit from opening long positions in stocks that are targeted by mergers and acquisitions.

A demotic example is when incomparable company buys some other that is listed connected a stock exchange. Let's say that Company A agrees to buy Company B for $10 a divvy up. Typically, until the deal is closed, the carry will trade at $9.75 on the securities market, not $10. It won't trade at $10 as there is a chance that the look at won't see.

The $0.25 represents a takeover arbitrage chance. A trader could corrupt the ancestry at $9.75 knowing that if the deal completes, they will gain $0.25 per parcel purchased. This is the matter-of-course restoration risk premium, or the compensation for attractive on the put on the line.

The risk is that the lot may not go through, in which shell Company B's share price falls back to where information technology was prior to the buy-out announcement. Some of the take a chanc could be outset by taking a dodge. A hedging strategy could personify to short the acquiring company (Party A) or buy a put option on Company B, assuming that the bounty doesn't offset the entire potential gain.

Seamlessly open and accurate trades, track your progress and set up alerts

Set income arbitrage

Fixed income arbitrage is a strategy that can exist victimized by traders for fixed income securities, so much as stocks and bond trading, with the aim of profiting from the divergence in interest rates. Institutional traders can also employ this method in more complex rate of interest products.

As an model, let's enunciat that two cities offering municipal bonds. The cities consume very synonymous economies, debt loads, revenue, expenses, and unemployment rates. I bond has a yield of 3%, while the other has a yield of 2.85%. A monger believes that the two bonds should payoff the same. Therefore, they short the 3% bond and buy the 2.85% surrender hamper. If they are correct and the bring together yields eventually align, whether rising, falling, or merging in the middle, the trader wish net income from the 0.15%.

The aforementioned construct could enforce to companies that issue bonds. If the companies are similar, only the bonds offer different rate of interest yields, in that location may be an arbitrage chance. A trader could forgetful the "expensive" succumb and buy the "under-priced" financial asset.

The gamble is that the yields exercise not converge or the spread gets even wider. In the last mentioned case, the dealer will pop out to lose money.

Covered interest arbitrage

Covered interest arbitrage exploits the differences of interest rates of adventive currencies 'tween countries. This is carried out direct futures or gardant contracts systematic to reduce rate of exchange hazard.

The forward grocery accounts for interest rate differences between currencies. If the forward market doesn't accurately ingredien the difference in pastime rates, then a trader could profit at the expiration of the forward contract.

Covered interest arbitrage involves a number of steps in order to net. Uncovered interest arbitrage is less complex but comes with more risk. With an uncovered strategy, there is no forward contract, so a trader is only borrowing in a lower rate currentness and investing in a higher rate currency. This works if the high interest rate currency doesn't drop to a greater extent than the interest rate differential. If it does, the practice loses money because, when funds are born-again back, they will be little than the avant-garde lend come.

Arbitrage calculator

An arbitrage reckoner, or arb calculator for short, calculates what the theoretical Price of an asset should beryllium supported on early inputs and how very much you should stake connected a trade to guarantee net income.

For instance, a triangular arbitrage computer requires the prices from cardinal currency pairs to calculate the fair damage of the third. If the real market price is different, the trader can decide if this is a tradable arbitrage opportunity.

While an arbitrage calculator likely has some sophisticated programming behind information technology, traders are cautioned to understand the math behind the calculation. For example, if the calculator is rounding, this could eliminate or increase the measure of arbitrage. Therefore, consider threefold-checking the maths before relying on third-political party calculations.

How to do arbitrage trading

- Compare the asset's market price to the projected or arts price/disposition, or possibly to other comparable assets.

- Calculate the latent profit from the arbitrage trade.

- Deduct fees and dealing costs. Consider spreads, commissions, and interest group costs.

- Consider the risks and employ a suitable risk management scheme to help your trade.

- Double ensure the maths and be after how the trades leave comprise executed. Write information technology down, so ideally take up all the orders ready to execute at the same clip, if possible.

Arbitrage platform

Victimisation our online trading platform, Next Generation, you force out make use of half-witted arbitrage strategies, such as pairs trading, asset correlations for hedging and forward contracts, which are available across multiple markets and instruments. A particularly popular form of arbitrage trading is scalping, which is commonly practised on our platforms past both retail and institutionalised traders. Learn much around the best tips and strategies for forex scalping.

Automated arbitrage trading

You can also try out automated arbitrage strategies using our international hosted platform, MetaTrader 4 (MT4), which provides the prospective for recursive trading through the use of Expert Advisors (EAS). These programs fundament be created Beaver State downloaded by the platform to search for arbitrage opportunities.

When using an automated program to trade, it is essential to monitor its performance and understand how it functions. Such programs could include coding or mathematical errors that could result in losing money. It is important that a monger coiffe their possess due application in front deploying any automated trading programs. Register for an MT4 account now.

Risks of arbitrage trading

Arbitrage trading is often said to be a risk-free profit, yet that is rarely legitimate. Most types of arbitrage create some rather risk, even if that gamble is someone-inflicted. For instance, a trader will typically desire to at the same time lock away all arbitrage trades. If orders are staggered, prices commode change and the arbitrage Crataegus laevigata personify lost.

E.g., in a triangular arbitrage switch, prices are constantly flowing 24-hours per day, in railway line with forex market hours. If an opportunity for arbitrage is found, all orders should constitute dead at the same prison term. Failure to do thusly means that each price is changing before the next order goes out, and any calculations in regards to the arbitrage may no more apply.

Other risks include using poor, confused, operating room insufficient information. This could apply to a applied math arbitrage swop. Two currency pairs may of late appear correlated, but then diverge. Therefore, the tradability depends on how long the correlation lasted and how likely those assets are to be correlated again in the future.

In generic, dealing costs, spreads, and commissions are forever a run a risk when spread betting or trading CFDs. Read more about our trading costs that should be taken into consideration before inaugural or placing a swap.

Disclaimer: CMC Markets is an execution-only avail supplier. The material (whether Beaver State not it states any opinions) is for general information purposes sole, and does not allow your grammatical category circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or else advice connected which reliance should glucinium placed. No opinion presumption in the material constitutes a testimonial by CMC Markets operating room the author that any particular investment, security, transaction or investment funds scheme is suitable for any specific somebody. The material has not been prepared in accordance with statutory requirements planned to promote the independence of investment explore. Although we are not specifically prevented from dealing before providing this material, we do not seek to capitalise of the material preceding to its dissemination.

finc-gb 3181 arbitrage trading strategies

Source: https://www.cmcmarkets.com/en-gb/trading-guides/arbitrage-trading

Posted by: diggstagathe.blogspot.com

0 Response to "finc-gb 3181 arbitrage trading strategies"

Post a Comment